How to Manage Car Expenses: Your 2026 Budget Guide

Managing car expenses is the process of budgeting and controlling all costs tied to vehicle ownership, including maintenance, fuel, insurance, taxes, and financing. Most drivers underestimate what their car actually costs because they focus on the monthly payment and ignore everything else. The full picture includes registration fees, depreciation, parking, and the repairs that hit without warning. This guide walks you through how to manage car expenses category by category, with real 2026 cost data, proven savings strategies, and tools like Carjourney, GasBuddy, and insurance comparison platforms to keep your budget on track.

How to manage car expenses with a realistic budget

Building a car budget starts with one rule: total car costs should not exceed 10% to 20% of your gross monthly income. For a household earning $100,000 per year, that means keeping all vehicle-related spending under $10,000 annually. That number covers more than your loan payment.

Your budget needs to account for every recurring and irregular expense. The main categories are:

- Loan or lease payment: Your fixed monthly obligation

- Insurance: Varies by driver profile, vehicle, and coverage level

- Fuel: Based on your average monthly mileage and local prices

- Maintenance and repairs: Oil changes, tires, brakes, and unexpected fixes

- Registration and taxes: Annual fees that vary significantly by state

- Parking and tolls: Often overlooked, especially for urban drivers

- Depreciation: The real cost of ownership that never shows up on a bill

Irregular costs are where most budgets fall apart. Registration fees, annual inspections, and tire replacements do not arrive monthly, so they feel like surprises. The fix is to divide their annual cost by 12 and set that amount aside each month in a dedicated savings account. A $600 tire replacement becomes $50 per month when you plan for it.

Pro Tip: Use Carjourney’s maintenance budget tools to set annual cost targets by category and get alerts when you are approaching your limits. It removes the guesswork from irregular expenses.

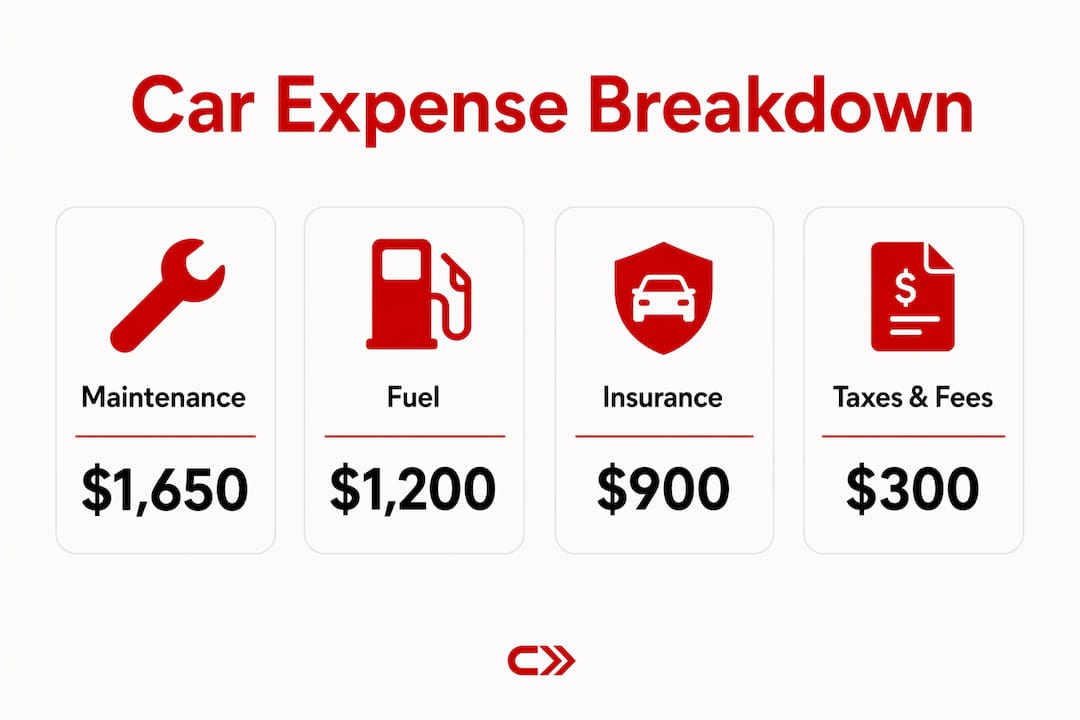

For 2026, car maintenance and repairs average about 11 cents per mile, which works out to roughly $1,650 per year for a driver covering 15,000 miles. Use that figure as your baseline when building the maintenance line of your budget, then adjust up for older or high-mileage vehicles.

What are the best strategies to reduce maintenance and repair costs?

Preventive maintenance is the highest-return financial decision you can make as a car owner. Preventive maintenance returns $2 to $5 for every $1 spent by preventing the costly repairs that deferred service causes. Skipping an oil change to save $80 today can lead to engine damage costing thousands later.

Here is a practical approach to keeping maintenance costs under control:

- Follow your mileage-based service schedule. Carjourney’s mileage-based maintenance guide maps out exactly what your vehicle needs at each interval, so you never miss a service that protects a major component.

- Prioritize oil changes above everything else. Deferred oil changes can lead to engine repairs costing up to $6,800, compared to $60 to $120 per service. The math is not close.

- Use independent mechanics for routine work. Dealership labor rates run 30% to 40% higher than independent shops for identical services. Reserve the dealer for warranty work and specialized diagnostics.

- Build a repair emergency fund. Set aside $50 to $100 per month specifically for unexpected repairs. When the alternator fails or a brake caliper seizes, you pay cash instead of putting it on a credit card at 20% interest.

- Learn basic DIY maintenance. Air filter replacements, wiper blades, and cabin filters are straightforward tasks that dealers charge $50 to $150 to perform. YouTube and your owner’s manual make these accessible to most drivers.

- Choose vehicles with strong reliability records. Toyota, Honda, and Mazda consistently rank lowest for repair frequency and cost in long-term ownership studies. Your vehicle choice at purchase sets your maintenance cost ceiling for years.

Pro Tip: Log every service in Carjourney so the AI can flag upcoming needs based on your actual mileage, not a generic schedule. It also stores your receipts digitally, which matters when you sell the vehicle.

Tracking your maintenance history is not just about staying organized. A complete service record adds measurable resale value and proves to buyers that the car was cared for properly.

How does driving behavior affect your fuel costs?

Fuel is one of the few car expenses you can reduce immediately without spending money. Aggressive driving reduces fuel efficiency by 15% to 33% on highways and 10% to 40% in city traffic, costing the average driver up to $960 per year in wasted fuel. That is a meaningful number that requires zero investment to recover.

The driving habits that cut fuel costs most effectively include:

- Smooth acceleration and braking. Hard starts and late stops burn significantly more fuel than gradual speed changes. Anticipate traffic flow and coast toward stops instead of braking hard.

- Maintaining proper tire pressure. Under-inflated tires increase rolling resistance and reduce MPG. Check pressure monthly and before long trips.

- Using the recommended fuel grade. Most vehicles run fine on regular unleaded. Using premium in a car that does not require it wastes money with no performance benefit.

- Reducing highway speed. Fuel consumption rises sharply above 60 mph. Dropping from 75 to 65 mph on a long trip produces measurable savings.

- Minimizing idle time. Modern fuel-injected engines use less fuel restarting than idling for more than 60 seconds.

GasBuddy is the most practical tool for finding the cheapest fuel near you. The app crowdsources real-time prices from stations in your area and can save $5 to $15 per fill-up depending on your market. Over a year, that compounds into real money.

EcoDriving techniques require no investment but can substantially reduce fuel costs and emissions. If you drive a plug-in hybrid or EV, charging at home during off-peak hours typically costs 40% to 60% less than public fast charging. Factor that into your fuel budget comparison if you are considering a vehicle switch.

How can you lower insurance and financing costs?

Insurance markets use price optimization that penalizes loyalty. Staying with the same insurer year after year typically results in higher premiums than new customers pay for identical coverage. Shopping your policy every two to three years can save approximately $450 per year. That is not a small amount for a 30-minute task.

The most effective strategies for reducing insurance costs are:

| Strategy | Estimated annual savings |

|---|---|

| Shop and switch insurers every 2 to 3 years | Up to $450 |

| Raise deductible by $1,000 | $509 to $636 |

| Bundle auto with home or renters policy | $150 to $300 |

| Drop collision coverage on older vehicles | Varies by vehicle value |

| Maintain a clean driving record | 10% to 20% discount eligibility |

Raising your deductible is one of the most direct levers available. Every $1,000 increase in deductible lowers annual premiums by 20% to 25%, saving approximately $509 to $636. The trade-off is that you need that deductible amount available in savings before a claim. Build the emergency fund first, then raise the deductible.

On the financing side, the interest rate and loan term you accept at purchase have a larger impact on total cost than most buyers realize. A longer loan term lowers your monthly payment but increases total interest paid significantly. Refinancing a car loan at 2 or more percentage points below your current rate can save over $1,000 across the loan term and reduce your monthly payment. If rates have dropped since you financed, contact your bank or credit union and ask for a refinance quote.

Pro Tip: Separate your insurance shopping from your renewal date. Insurers know you are less likely to switch when you are busy with renewal paperwork. Set a calendar reminder 60 days before renewal to get competing quotes.

What hidden costs do most car budgets miss?

Most overspending occurs after purchase on insurance, financing, and maintenance rather than on the vehicle price itself. But three categories consistently fall outside standard budget templates: registration and taxes, parking and tolls, and depreciation.

Registration fees and property taxes vary dramatically by state. Virginia charges an annual personal property tax on vehicles based on assessed value. Texas charges no such tax but has higher registration fees. Before buying a vehicle, look up your state’s annual registration and tax obligations for that specific make, model, and year.

Monthly parking fees range from $50 in suburban areas to over $400 in dense urban markets, with tolls adding another $20 to $200 per month. A driver commuting into Washington, D.C. or New York City can easily spend $4,000 to $7,000 per year on parking and tolls alone. That figure belongs in your car budget, not your miscellaneous spending category.

Depreciation is the largest single cost of car ownership for most drivers, yet it never appears on a monthly statement. New vehicles lose 15% to 25% of their value in the first year. Buying a 2 to 3 year old used car saves roughly $14,000 to $15,000 compared to buying new by letting the first owner absorb that loss. If you are buying new, factor depreciation into your true cost of ownership calculation, not just your monthly payment.

Key takeaways

Managing car expenses effectively requires budgeting for every cost category, applying preventive maintenance, shopping insurance regularly, and tracking all spending with a dedicated tool.

| Point | Details |

|---|---|

| Use the 10% to 20% income rule | Keep total car costs under 20% of gross monthly income to maintain financial stability. |

| Preventive maintenance pays off | Every $1 spent on routine service returns $2 to $5 by preventing major repairs. |

| Shop insurance every 2 to 3 years | Loyalty penalties cost drivers up to $450 per year in unnecessary premium increases. |

| Budget for hidden costs | Registration, parking, tolls, and depreciation add thousands annually and belong in every car budget. |

| Track expenses consistently | Logging every cost in a tool like Carjourney reveals patterns and prevents budget drift over time. |

Why I stopped treating car costs as fixed expenses

The shift that changed how I manage vehicle costs was simple: I stopped treating car expenses as fixed and started treating them as a system I could influence. Most drivers accept their insurance renewal, pay whatever the dealer quotes for service, and fill up at the nearest station. Each of those defaults costs real money.

The drivers I see managing auto expenses well share one habit. They review their full vehicle cost picture at least once a year, not just their loan payment. They know their cost per mile, their insurance renewal date, and roughly what their next major service will cost. That awareness alone prevents most of the financial surprises that make car ownership feel expensive.

The mistake I see most often is skipping preventive maintenance to save money in the short term. A $120 oil change feels optional when money is tight. A $6,800 engine repair is not optional. The math on preventive maintenance is not subtle. It is one of the clearest financial decisions in personal finance.

My other strong recommendation is to use a car ownership cost tracker from day one with any vehicle. Not a spreadsheet you will abandon in February. A tool that connects to your actual service history and reminds you what is coming. The difference between reactive and proactive car ownership is almost entirely about information.

— Chally

Take control of your car costs with Carjourney

Carjourney is built for drivers who want to stop guessing and start knowing exactly what their vehicle costs. The platform uses AI to scan your service documents, track your maintenance history, and flag upcoming expenses before they catch you off guard. You get a clear picture of your yearly maintenance costs and spending trends in one place, without digging through receipts or spreadsheets. Whether you are managing a daily driver or a weekend build, Carjourney connects your real service data to a community of enthusiasts and AI-powered insights that generic apps cannot match. Visit Carjourney to start tracking your vehicle costs today.

FAQ

What percentage of income should go to car expenses?

Total car-related expenses should stay between 10% and 20% of your gross monthly income. For a $100,000 annual salary, that means keeping all vehicle costs under $10,000 per year.

How much should I budget for car maintenance per year?

Car maintenance and repairs average about 11 cents per mile, which equals roughly $1,650 per year for 15,000 miles driven. Older and higher-mileage vehicles will run higher than that baseline.

How do I save on car insurance without reducing coverage?

Shop your policy with competing insurers every two to three years, raise your deductible if you have savings to cover it, and bundle your auto policy with home or renters insurance. These three moves alone can save $600 or more annually.

What is the best way to track car expenses effectively?

Use a dedicated app like Carjourney that logs service records, stores receipts, and tracks spending by category. Spreadsheets work but require manual discipline that most drivers do not sustain long term.

Does buying used really save money on car costs?

Buying a two to three year old used vehicle saves roughly $14,000 to $15,000 compared to buying new by avoiding first-year depreciation. It is one of the highest-impact financial decisions in vehicle ownership.